Description

Alternative Tests - FasterCapital

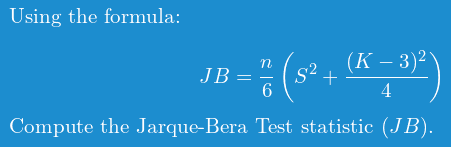

Jarque-Bera Test: Guide to Testing Normality with Statistical

Are financial time series (investment returns) stationary

Jarque-Bera Normality Test

Normality Assumption - FasterCapital

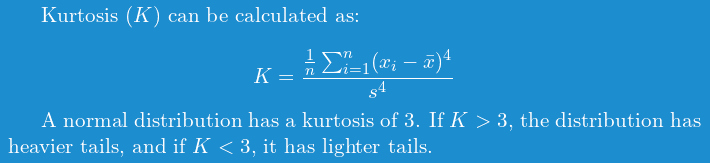

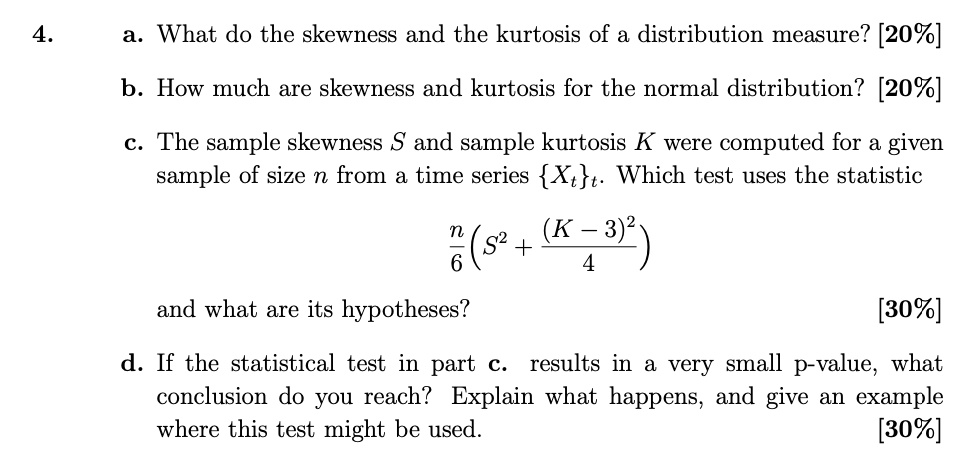

SOLVED: 4. a. What do the skewness and the kurtosis of a

/probability_distribution_function_plots.png)

Information Demand and Stock Return Predictability (Coded in R

Jarque-Bera Test for Asset Returns 7

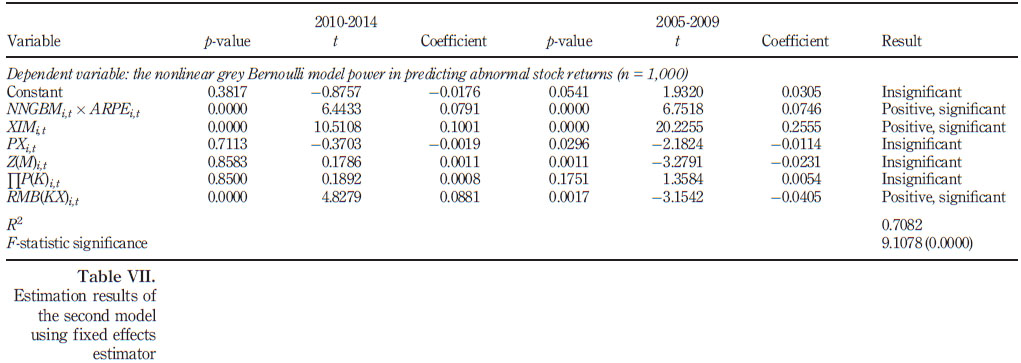

Modeling and forecasting abnormal stock returns using the

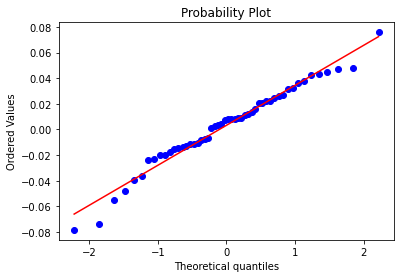

Test for Normality Using Python: Complete Guide - PyShark

A Guideline for Running Regression

Likelihood Ratio Tests: Fractionally Integrated (FI) versus

Jarque-Bera Test: Guide to Testing Normality with Statistical

Related products

Silver and Silver Vermeil Ring Dragon-fly motif TOUS Real Mix Bera

India, Rajasthan state, Bera area, Alexandrine Parakeet or Alexandrian Parrot (Psittacula eupatria) - SuperStock

India Rajasthan state Bera area temple in the mountain pilgrims Stock Photo - Alamy

Maya Bera, Senior Computer Specialist, Yoram Rudy Lab

$ 20.99USD

Score 4.5(470)

In stock

Continue to book

$ 20.99USD

Score 4.5(470)

In stock

Continue to book

©2018-2024, followfire.info, Inc. or its affiliates